There’s a lot of noise out there drowning out an important signal most Americans should probably know about (yes, even MAGA! Perhaps especially MAGA given the disproportionate effects this Republican budget bill is likely to have on their red state communities). That is by design — retired entrepreneur Bill Southworth refers to it as “narrative warfare” in the Russian tradition; Steve Bannon calls it “flooding the zone with shit;” and psychologists simply call it narcissistic personality disorder. By whatever name, today’s political information ecosystem is being manipulated to obscure the actual business of government, because the culture wars are staggeringly popular while the actual GOP agenda goes over like a lead balloon in terms of popular opinion.

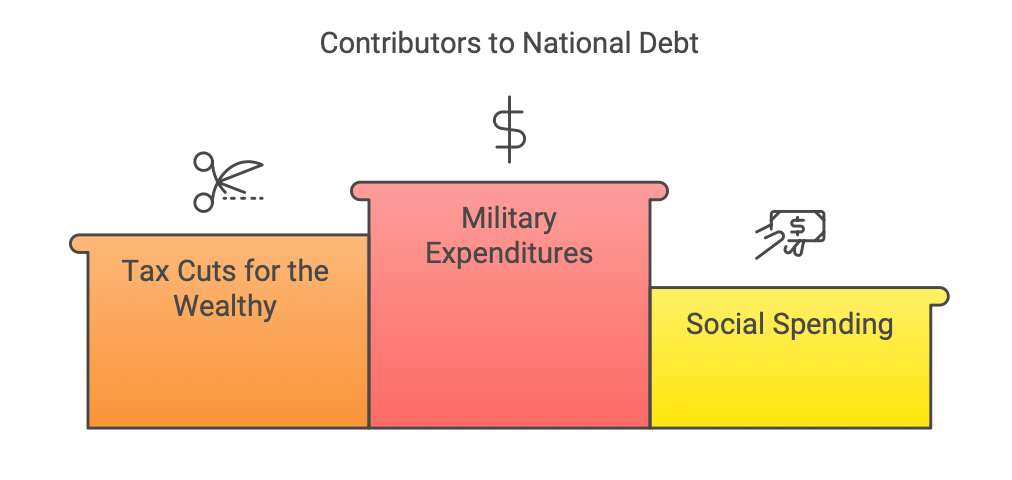

The reckless cuts to public services are meant to offset the cost of what Republicans and their billionaire donors want on the other side of the ledger: the extension of Trump’s 2017 tax cuts for their corporate donors and wealthiest Americans. Nevermind, apparently, that these tax cuts are primarily responsible (along with the George W. Bush tax cuts of the early 2000s) for the increasing debt ratio that the GOP falls all over themselves to theatrically complain about — while single-handedly and relentlessly continuing to make it worse.

The trajectory of the U.S. national debt is a compelling narrative that mirrors the nation’s evolving priorities, polarities, challenges, and triumphs. From the nascent days of the republic, grappling with the financial aftermath of the Revolutionary War, to the expansive fiscal policies of the 20th century, each era offers a unique lens into the economic and political forces at play in the history of the national debt.

In the late 18th century, under the stewardship of Alexander Hamilton, the United States established its first national debt—a strategic move to unify the fledgling states and build creditworthiness. The 19th century witnessed fluctuations driven by events such as the Civil War, which necessitated unprecedented borrowing, followed by periods of aggressive debt reduction during peacetime.

The 20th century introduced complexities with global conflicts like World War I and WWII, the Great Depression, and the Cold War, each leaving indelible marks on the nation’s fiscal landscape. Post-World War II prosperity facilitated debt reduction, but subsequent decades saw increases due to military engagements, economic policies, and social programs.

As we navigate the 21st century, the national debt continues to be a focal point of economic discourse, influenced by factors ranging from tax policies to global pandemics. Tax cuts for the wealthy under Reagan, the Bushes, and most notably Trump since 1980 have blown a hole in the debt. Military adventurism around the world including 2 completely unpaid for Gulf Wars in the ’90s and 2000s and the 20-year war in Afghanistan ballooned it as well.

This timeline delves into the pivotal moments that have shaped the U.S. national debt, offering insights into the decisions and events that have influenced its rise and fall over the centuries — so we can get intimately familiar with which policies increase or decrease it.

At least, not according to what Republicans promised when they passed them. The Trump tax cuts didn’t work to grow the economy, increase revenues, alleviate the debt, or benefit ordinary Americans as alleged.

The Tax Cuts and Jobs Act (TCJA) was introduced by then-Speaker of the House (and fiscal hawk) Paul Ryan and signed into law by then-President Donald Trump on December 22, 2017. It permanently reduced the corporate tax rate from 35% to 21%, and lowered the overall tax for all brackets — seems fair, right? Except the wealthy walked away with 50 times the amount of tax benefit as the lower brackets.

Trump tax cuts add $1.5 trillion to the deficit

Not only did the tax cuts not raise revenue as promised — they became a liability on the balance sheet when almost immediately going into the red. The Joint Committee on Taxation (JCT) estimated the TCJA would add approximately $1.5 trillion to the federal deficit over 10 years, after accounting for any temporary growth effects. The national debt will rise to accommodate as we borrow money to make up the shortfall between earnings and expenditures.

The Trump tax cuts reduced federal tax revenue, with significant declines in corporate tax receipts (surprise, surprise!). They did the exact opposite of what they promised to do — leaving our economy in a more precarious position even before the pandemic hit.

Who benefited from Trump’s tax cuts?

Conservatives and right-wing economists claim that tax cuts will help ordinary people by raising wages. In reality, however, corporations instead used their tax windfalls to do other things: stock buybacks, dividends, and executive pay. In fact, this happens over and over again each cycle of empty promises from so-called “fiscal conservatives” who in large part know exactly what they do.

They seem to believe they are entitled to the lion’s share of America’s money (as they have been since at least Mudsill Theory in 1858 and even before) and by gum, nothing is going to stop them — not democracy, not a sense of decency, not a sense of institutional preservation as used to be the very core pillar of Conservatism. No longer. Now it’s a will to power and to plunder. It’s not so much trickle down as it is hoover up.

Reaganomics, Trickle down, Laffer curve, Supply-side economics — it’s all the same

The magical revenue-generating power of tax cuts has been long promised and never delivered by right-wing Republicans. Since the 1980s edition, Reaganomics — the economic “theory” drafted on the back of a cocktail napkin dubbed the Laffer Curve for the slightly drunken man who scribbled it — has moved immense amounts of wealth upwards into the hands and coffers of the 1% and 0.1% at the expense of the masses.

The argument is that rich people will take the extra billions in returned tax money and use it to innovate and grow the economy — except that never happens. And why would they? They don’t have to earn revenue the old-fashioned way, through free market competition — they can just sit back on their laurels, buy a Senator or two, and rake in a huge windfall every few years that a GOP officeholder is in the White House. It is rock solid orthodoxy for the right-wing now, that tax cuts are almost the only policy initiative they care about — along with a side of deregulation and the slashing of the social safety net.

We’ve seen this movie before. The rich guys take the money and run — in many ways literally, into the arms of tax-free havens like the Cayman Islands or Seychelles. They do not return it to the American economy — although they do inject it into American politics, to skew the playing field even further in their favor despite already extracting extraordinary privileges and benefits to themselves from all aspects of their coziness with the political elite and their direct capture of various institutions.

As LBJ once said:

“If you can convince the lowest white man he’s better than the best colored man, he won’t notice you’re picking his pocket. Hell, give him somebody to look down on, and he’ll empty his pockets for you.”

President Lyndon Baines Johnson, 1960

The economic elites are dividing us over race and religion, in order to pick our pockets. This is why we can’t have nice things. We should boot them out and have nice things.

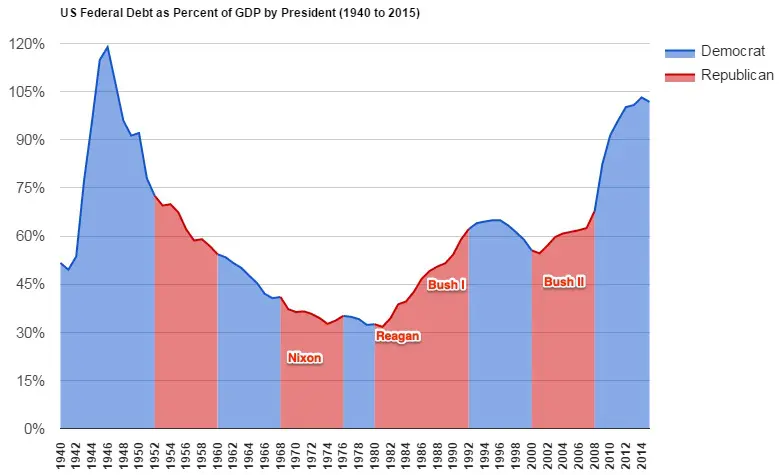

Mythology has it that “reckless Democratic spending” is to blame for the ballooning of the national debt — though the historical record shows otherwise.

In fact, the conservatives‘ beloved demi-god Ronald Reagan was the first President to skyrocket the debt, thanks to some bunk ideas from an old cocktail napkin that linger to this day — the Republican monetary theory in a nutshell is (I shit you not) that we should take all our pooled tax money and give it to… billionaires. Because, you know, they’re clearly the most qualified people to make decisions affecting the 99% poor people. Supposedly they’re the smartest folks to entrust with our money.

Trickle down, debt up

Except it’s not true, as year after year and study after study shows. Nor for all their finger-waggling at Democrats over the national debt has the GOP turned in a balanced budget since Nixon. Republicans are the most gigantic hypocrites on economics writ large, but particularly so for the national debt — with Reagan, Bush I, Bush II, and Trump all turning in record debt increases, primarily through tax cuts for the wealthy and the Gulf and Afghanistan wars.

Meanwhile, Bill Clinton balanced the budget, created a surplus, and reduced the debt during his 8 years in office, and Obama inherited the deepest recession since the 1929 Great Depression.

The financial crisis of 2008-09, itself caused by the reckless Republican zeal for deregulation — this time of financial derivatives — was a wholly GOP-owned debacle that the next president paid for politically. Nevertheless, President Obama had the debt again on a reduction path as a percentage of GDP — but then Donald “I bankrupted a series of casinos!” Trump oozed his way into the highest office in the land.

It’s weird how “reckless Democratic spending” always happens under Republican administrations!

During the Trump administration, Republicans patted themselves on the back for giving a $2.7 trillion tax cut to billionaires for no reason, while the economy was relatively hot already (after being rescued by Obama). Not only was no progress made on diminishing the debt, but the national debt actually increased (both nominally and as a percentage of GDP) under Trump’s first term even before the sudden arrival of a novel coronavirus caused it to leap into the stratosphere like a 21st century American tech oligarch.

Only when President Biden arrived on the scene and took the helm of fiscal and monetary policy did the national debt begin cooling off once again — all while dramatically and quickly scaling up covid-19 vaccine production and distribution and passing over $3 trillion in Keynesian legislation meant to get the dregs of the middle class reoriented to a place on the map vis-a-vis the 1% once again.

Republican national debt bullshit

I am hereby calling bullshit on Republicans’ crocodile tears over the national debt, which they suddenly remember only when a Democrat is in town and summarily ignore while their guy is in the hot seat burning through cash like it’s going out of style.

We need to have a better collective narrative for Democratic success on the economy. The Republicans are no longer the kings of the economic world — if they ever were. It feels more like smoke and mirrors each passing day, with climate change denial, the Inflationary Boogeyman, and other GOP Greatest Hits playing ad nauseum on the AM social media waves.

Here are at least a few things to remember about the national debt, that Republicans generally get wrong:

wars are very expensive

booms in social services are expensive too; but not as expensive as wars

there is not any perceivable truth in the old GOP party line that Democrats always overspend and Republicans are always thrifty

Reagan and both Bushes presided over two of the biggest spikes in public debt in recorded history, outside of FDR who had both the Great Depression and WWII to contend with

Clinton, Carter, Johnson, Kennedy, and Truman all decreased the debt

be wary of graphs that don’t “normalize” to GNP — it’s an attempt to “lie with statistics” by obfuscating the roles of inflation and the growth of the economy itself

there is more than one way to look at and evaluate the level of public debt