Why Healthcare Costs Stay High—And How the ACA Actually Helps Lower Them

America’s health care cost problem has a perverse logic at its core: we’ve committed to providing emergency care to everyone who needs it, regardless of ability to pay — but we’ve historically failed to ensure people have access to the preventive and primary care that would keep them out of astronomically expensive emergency rooms in the first place.

This contradiction creates a predictable—and expensive—spiral. Uninsured patients, lacking regular access to doctors, delay care until conditions become acute. They end up in emergency departments, where hospitals are legally required to treat them under EMTALA (the Emergency Medical Treatment and Labor Act — signed into law by Ronald Reagan in 1986). Those visits generate massive uncompensated costs that hospitals pass along to everyone else: insured patients through higher prices, insurance companies through higher premiums, and taxpayers through increased public spending.

The Affordable Care Act was designed, in part, to break this cycle by attacking the problem at its source. The logic is straightforward: expand insurance coverage, and you enable people to seek preventive and primary care before minor issues become medical emergencies. Fewer emergency visits mean less uncompensated care, which translates to lower costs for hospitals, taxpayers, and the broader healthcare system.

And the data backs this up. Research consistently shows that after the ACA’s implementation, emergency department visits by uninsured patients declined significantly. More people with insurance meant more people managing chronic conditions, catching health problems early, and avoiding the emergency room when they had other, more appropriate care options. The shift from reactive emergency care to proactive preventive care doesn’t just improve health outcomes—it fundamentally reduces the financial burden on everyone in the system.

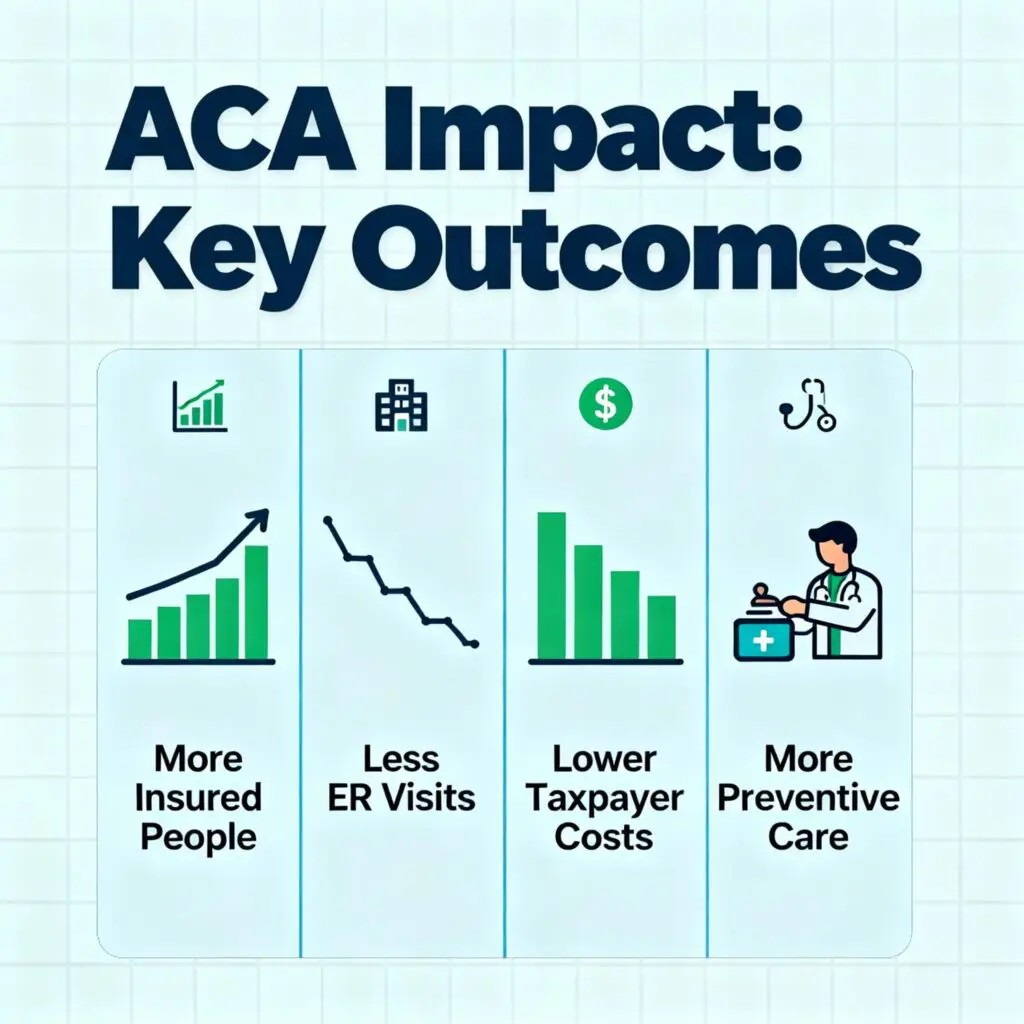

The image above captures the four key outcomes: more insured people leading to fewer ER visits, lower taxpayer costs, and increased preventive care. Understanding this mechanism reveals why expanding coverage isn’t just a moral imperative—it’s a rational economic policy that makes the system work better for everyone, including those already insured.

But how exactly does this work in practice? And if the ACA helps lower costs, why don’t more people understand this benefit? Below, we answer the most common questions about healthcare costs, the hidden “emergency room tax” that everyone was paying before the ACA, and why the law remains one of the most misunderstood cost-saving policies in American history.

Why is health care so expensive in America?

Because hospitals must provide emergency care to everyone under EMTALA (1986). When patients can’t pay, those uncompensated bills ripple into higher local taxes and insurance premiums. It’s the costliest way to fund care.

Doesn’t the government already cover emergency care?

Only partially. Before the ACA, much of the shortfall landed on cities, counties, and public hospital districts — i.e., local taxpayers.

How does the Affordable Care Act reduce those costs?

The ACA increases coverage through Medicaid expansion, marketplace plans, and income-based subsidies. With more people insured, hospitals face fewer unpaid ER bills, lowering systemwide costs that would otherwise hit your taxes and premiums.

Does the ACA actually lower my taxes?

Indirectly, yes. Less uncompensated emergency care means less public spending to backfill hospital losses, easing pressure on municipal and state budgets.

Why do premiums still feel high?

Provider prices, drug costs, and market forces still play major roles. The ACA didn’t set prices; it reduced the most wasteful cost center — unpaid emergency care — while strengthening rate review and marketplace competition.

How do deductibles fit into this?

Lower deductibles cost more upfront but cap financial risk. ACA cost-sharing reductions help eligible enrollees afford plans with manageable deductibles, reducing ER-driven debt and future taxpayer burdens.

What’s the bottom line?

- Emergency care is a legal public service. Funding it through last-resort ER visits is the most expensive way to do it.

- The ACA moves spending upstream — emphasizing prevention and coverage instead of crisis care — which cuts ER overuse, lowers premiums, and reduces hidden “emergency room taxes.”

Comments are closed.